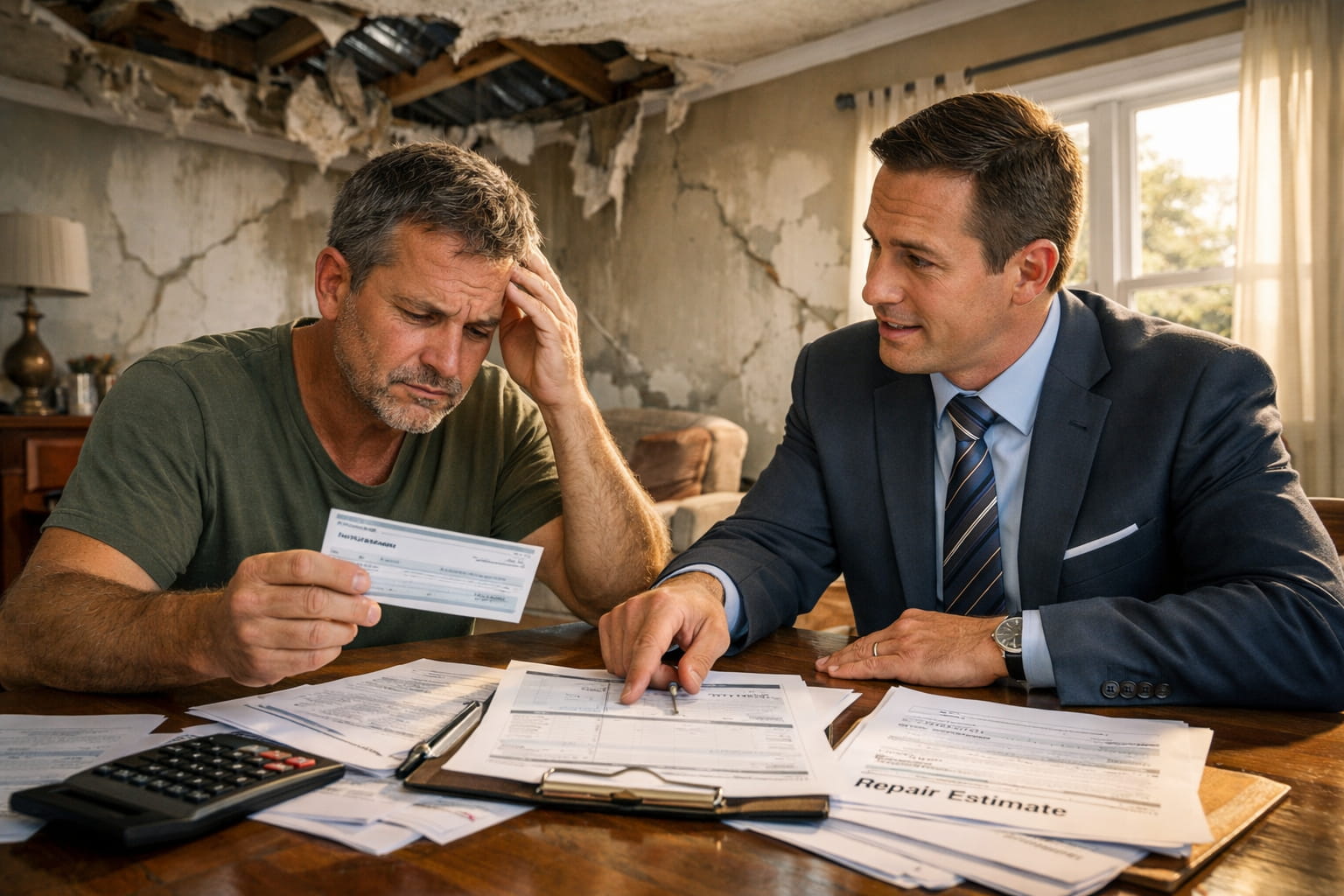

If you recently received a settlement check from your insurance company, you might assume the process is over. But for many homeowners across Bradenton, Sarasota, Venice, and Lakewood Ranch, that check is only the beginning of the problem. Insurance companies settle claims quickly, but that speed often comes at a cost to you.

Underpaid claims are one of the most common and least talked-about issues in Florida’s property insurance market. The insurer’s adjuster works for the insurance company. Their job is to process your claim within the insurer’s guidelines, not to maximize what you receive. That means missed damage, outdated pricing, and policy language that quietly reduces your payout.

Ryan Risteen and his team have spent years helping property owners on the Gulf Coast recover what they were actually owed. Here is what to look for if you suspect your claim fell short.

What Does ‘Underpaid’ Actually Mean?

An underpaid claim is not the same as a denied claim. Your insurance company acknowledged the damage and sent a check, but the amount was insufficient to cover the necessary repairs for your property.

A report from the Florida Office of Program Policy Analysis and Government Accountability found that homeowners who hired a water damage insurance adjuster in Bradenton, FL, received settlements significantly higher than those who handled claims on their own. This difference is not a coincidence; it reflects how claims are documented, measured, and negotiated. If you suspect your insurance claim in Florida has been underpaid, it’s essential to review the settlement carefully.

6 Signs Your Settlement Was Too Low

- The Insurance Adjuster Was at Your Property for Less Than an Hour

A thorough property inspection after a storm or water damage can take several hours. If the insurance company’s adjuster completed their review quickly, there is a strong chance they missed something. Roofs, attics, walls, and crawl spaces all require careful inspection. Rushing through that process leaves damage unaccounted for and directly impacts your settlement.

- Your Contractor’s Estimate Is Higher Than the Settlement

This is one of the clearest signs that something went wrong. If you hired a licensed contractor to assess your damage and their estimate is significantly higher than what the insurance company paid, that gap needs to be explained. More often, it means the insurer’s scope of work was too narrow, or their pricing was outdated.

- The Settlement Uses Actual Cash Value Instead of Replacement Cost

Most homeowners assume their policy covers full replacement costs. Many do. But insurance companies sometimes apply depreciation aggressively, paying only the ‘actual cash value’ of damaged materials rather than what it actually costs to replace them. If you have a replacement cost policy, your settlement should reflect current material and labor prices in the Sarasota-Bradenton market, not what your roof was worth a decade ago.

- Visible Damage Was Left Off the Estimate

Insurance adjusters are not always roofing or water damage experts. When they write up your claim, they may document the most obvious damage and miss secondary effects. Water damage can travel far from its source. Mold risk, structural damage, and interior moisture intrusion often appear weeks after the initial loss. If those were not documented early, they may have been excluded from your settlement.

- You Were Paid a Lump Sum With No Itemized Breakdown

You have the right to know exactly what your settlement covers. If your insurance company issued a check without a clear line-by-line breakdown of what was included, you have no way to verify whether every damaged item was accounted for. Ask for the full scope of the loss document. If critical areas are missing, that is grounds to push back.

- You Accepted the First Offer Without a Second Opinion

Insurance companies count on homeowners accepting the first offer. It feels official. It arrives on company letterhead. But it is not final. In Florida, you have legal options to reopen or supplement a claim within certain timeframes. If you accepted a settlement without consulting a licensed public adjuster, it does not necessarily mean you are out of options.

A Real Example From the Gulf Coast

One Phoenix Claims Consulting client received an initial storm settlement offer of less than $25,000 after Hurricane Milton caused significant damage to their home. Ryan Risteen, a licensed water damage insurance adjuster in Bradenton, carefully reviewed the claim, documented all previously overlooked damage, and negotiated directly with the insurance carrier, securing a final settlement exceeding $200,000.

That kind of gap does not reflect bad luck. It reflects the difference between a claim handled by a policyholder alone and a claim handled by an experienced public adjuster who knows exactly what to document and how to present it.

What a Public Adjuster Does That You Cannot Do Alone

Ryan Risteen is a licensed public adjuster. His job is not to file paperwork. It is to build the strongest possible case for your settlement. That includes:

- A thorough damage inspection using professional tools and methods

- A comprehensive scope of loss that accounts for all damaged systems, not just the visible ones

- Accurate pricing using current local labor and material rates in the Gulf Coast market

- Direct negotiation with the insurance company on your behalf

- Supplemental claims when additional damage is discovered after an initial settlement

Property owners in Sarasota, Bradenton, Venice, and Lakewood Ranch who work with Phoenix Claims Consulting pay nothing upfront. Ryan’s team is compensated as a percentage of the settlement they recover for you. If they do not recover more, there is no fee.

How Long Do You Have to Dispute an Underpaid Claim in Florida?

This is one of the most important questions to ask. Florida law sets deadlines for reopening claims and filing supplemental claims, and those timelines have changed in recent years due to legislative updates. Property owners generally have a limited window after a loss to pursue additional recovery.

Do not assume time has expired without checking. Ryan and his team offer free consultations and can quickly assess whether your claim is still within the filing window. The sooner you reach out, the more options you are likely to have.

Frequently Asked Questions

How do I know if my insurance claim was underpaid?

The clearest signs include a contractor estimate that exceeds your settlement, visible damage that was not listed in the insurer’s scope, or a settlement paid without a detailed breakdown. A licensed public adjuster can review your claim at no cost and tell you whether there is room to recover more.

Can I reopen an insurance claim after accepting a settlement in Florida?

In many cases, yes. Florida law allows for supplemental and reopened claims within certain timeframes. The specific deadlines depend on your policy and the date of loss. Contact a licensed public adjuster as soon as possible to find out whether your claim is still eligible.

Does hiring a public adjuster mean I have to go to court?

No. Most underpaid claims are resolved through negotiation and documentation, without litigation. A public adjuster handles the process on your behalf and only refers to an attorney when a claim genuinely requires legal action.

How much does it cost to hire a public adjuster in Florida?

Phoenix Claims Consulting works on a contingency basis. There are no upfront fees. Ryan’s team is paid a percentage of the additional recovery they secure for you, so there is no financial risk to getting a second opinion on your settlement.

What areas does Phoenix Claims Consulting serve on the Gulf Coast?

Ryan Risteen and his team serve homeowners and property owners throughout Bradenton, Sarasota, Venice, Lakewood Ranch, and the surrounding Gulf Coast communities.

Get a Free Review of Your Settlement

If your insurance settlement doesn’t feel right, don’t ignore it, trust your instincts. Ryan Risteen and his team at Phoenix Claims Consulting will thoroughly review your underpaid insurance claim in Florida, inspect your property if necessary, and provide a clear, honest assessment of your options.

Take action now to ensure you receive the full compensation you deserve. Contact us to get started today.

About the Author

Ryan Risteen is the owner and licensed public adjuster at Phoenix Claims Consulting, based in Bradenton, Florida. With over 17 years of experience representing Gulf Coast homeowners and property owners, Ryan and his team specialize in hurricane, storm, water, and fire damage insurance claims. State License #P172623.